PTP TR - Self Employment entries for Basis Period Reform with two sets of accounts

Article ID

kba-03850

Article Name

PTP TR - Self Employment entries for Basis Period Reform with two sets of accounts

Created Date

2nd September 2024

Product

Problem

Self Employment entries where there is a change of Accounting Period as a result of Basis Period Reform and there are two sets of accounts

Resolution

This example relates to a taxpayer who previously had a December year end so the last accounts were made up to 31/12/2022. The new year end is going to be 31st March and two sets of accounts have been produced. The following is the data entry required for the 2023-24 return. In this example there is a profit of £15000 for the 15 month period which we will split as £12000 for the first period and £3000 for the transition period.

1. The first Accounting Period is entered as 01/01/2023 to 31/12/2023

2. All data entry for ‘Income and Expenses’ and ‘Capital Allowances’, should relate to the first accounting period. In this example there is a profit of £12000 for the 12 month period.

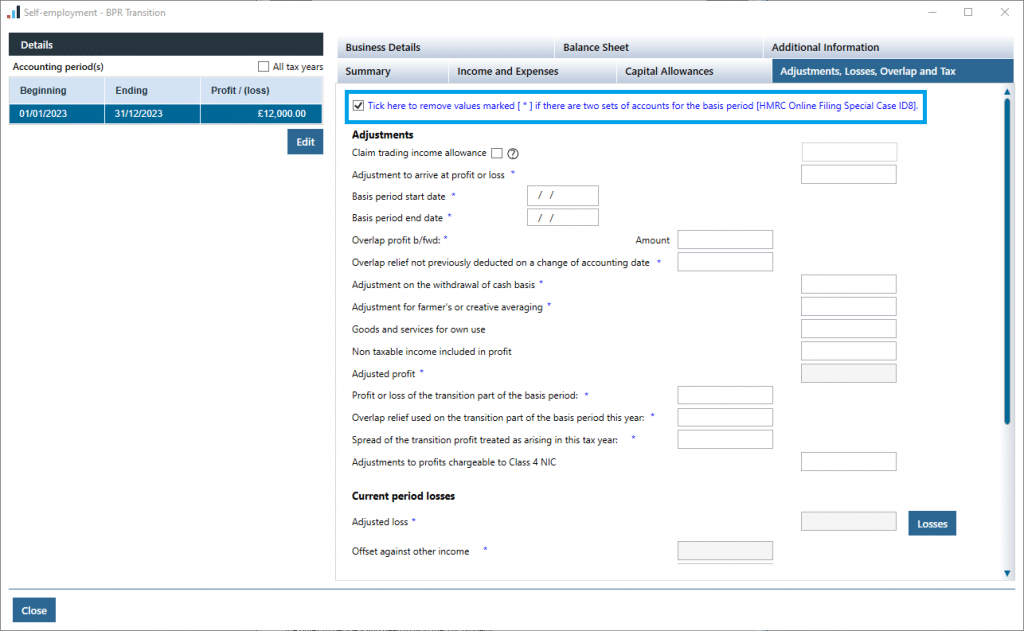

3. In the tab for ‘Adjustments, Losses, Overlap and Tax’ tick the box at the top “Tick here to remove values marked [*] if there are two sets of accounts for the basis period [HMRC. Online Filing Special Case ID8]”. This will remove most entries in this tab, including the Adjusted Profit figure.

4. A pdf document will open explaining more about the workaround for HMRC Special Case ID8. Please note this guide is generic for a change of accounting period, and not specific for Basis Period Reform. When it comes to making the adjustment on the second set of accounts please see the note at point 8 of this Knowledgebase article.

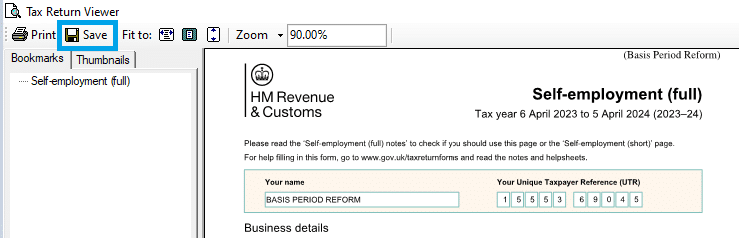

The next step is to print preview the first set of Self Employment pages and save a copy as a pdf file. The only selections should be for the Self Employment pages.

5. Select Save to save a copy of the Self Employment pages in a location of your choice

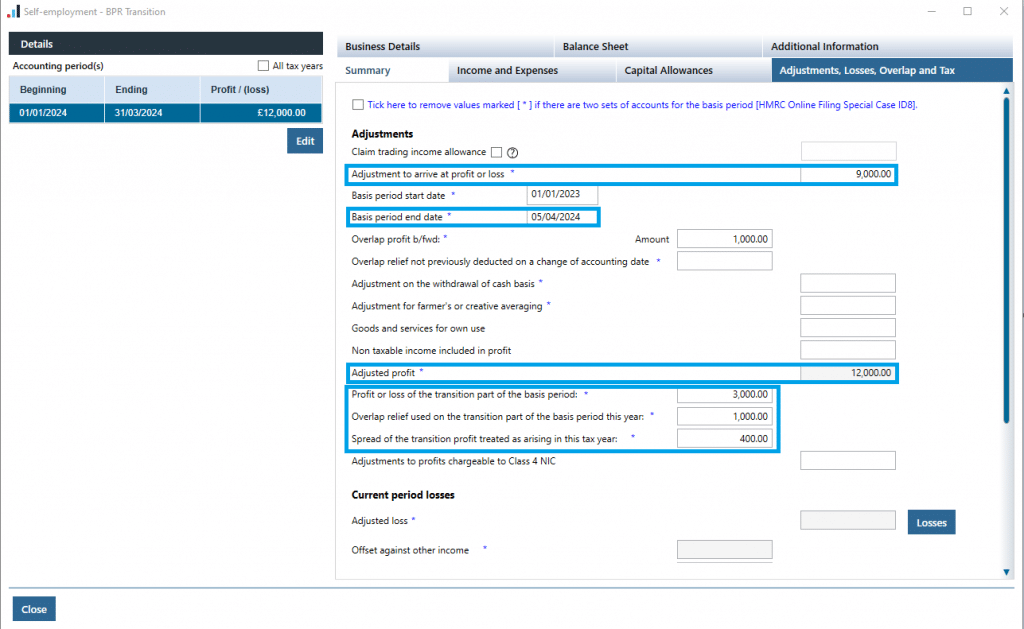

6. View the Tax Return and view the Self Employment pages once more. The workaround for Special Case 8 requires us to overtype the first period with the entries for the second period. Select Edit on the left hand side.

7. Select the Pencil icon to edit the Accounting Period dates and click OK. Then overtype/import the figures with those from the second set of accounts.

8. The Basis period end date is the end of the tax year 05/04/2024, even if the year end is 31/03/2024. An adjustment must be made in Adjustment to arrive at profit/(loss) so that the Adjusted Profit is the figure from the first set of accounts. In this example, we have £3000 of profit for the transition period so we need to enter an adjustment of £9000 to arrive at the expected Adjusted Profit of £12000.

9. The transition portion of the profit is entered in ‘Profit or loss of the transition part of the basis period’

10. Any overlap relief to be deducted is entered in ‘Overlap relief used on the transition part of the basis period this year’. (Please note if the overlap relief b/fwd is higher than the transition profit, the higher figure should be entered here and the software will automatically utilise the remainder against the standard part of the profit.)

11. The ‘Spread of the transition profit treated as arising in this tax year’ must be a minimum of 20% of the ‘Profit or loss of the transition part of the basis period’ minus ‘Overlap relief used on the transition part of the basis period this year’, but a higher figure could be entered if desired.

12. Within the Tax Calculation Summary, the Standard Profit and Transition Profit will show in separate places. Only the Standard Profit will be listed in the Income section at the top. The Transition Profit shows as part of the tax calculation breakdown below.

13. During the FBI process, attach the pdf of the first set of accounts which was saved during step 5.

We are sorry you did not find this KB article helpful. Please use the box below to let us know how we can improve it.